How To Retire On $250,000 With Cryptos (And Still Earn $100,000 Annually)

Yield Farming Lesson #7

People are attracted to cryptocurrencies for two main reasons: (1) the prospect of building enough wealth to live well and (2) the prospect of retiring well. This lesson is focused on the second of those aims (though it helps with the first too).

Here’s the basic idea.

If you deposit your stable coins (USDC and equivalents) in the right places, then by using a conservative estimate you can earn 40% in a year on that. This means that with $250,000 and this strategy, you’ll be able to live on $100,000 each year. Indefinitely.

I know. It sounds too good to be true. So, let’s jump right into that.

What’s The Catch?

I think there are two caveats, not exactly catches, involved here.

The first is that for this to work, you are going to have to deposit your $250k and wait around a year to recover your first $100k to live on. If you do it sooner than that, you won’t get as much money because you’ll be eroding your principal investment.

The good news is that you can keep your $100k in an account like Crypto.com and earn 10% - 13.5% interest if you make monthly withdrawals. That’ll help to pay taxes too.

The second is that you need to keep on top of things. This isn’t the sort of investment where you deposit and forget. You’ll need to do bi-weekly monitoring to know if you need to move your money around for higher yields.

Paid subscribers —DIY-ers, Crypto Riders, and Bubble Riders will get those updates from me. So for $15 a month, you won’t have to do all that leg work.

Tim Ferriss became famous for his 4 Hour Workweek. Well, this proposal is the 2 Hour Workweek. Yes, it’s still some work, but it’s not a job.

So those are the caveats. They are manageable though. Now let’s turn to the risks, which also prove manageable.

What Are The Risks?

In a previous Lesson in the Yield Farming series, I distinguished between two main types of risk. In this one, we’ll need to refine those distinctions a bit more to ensure that we get the results desired.

Investment Risk

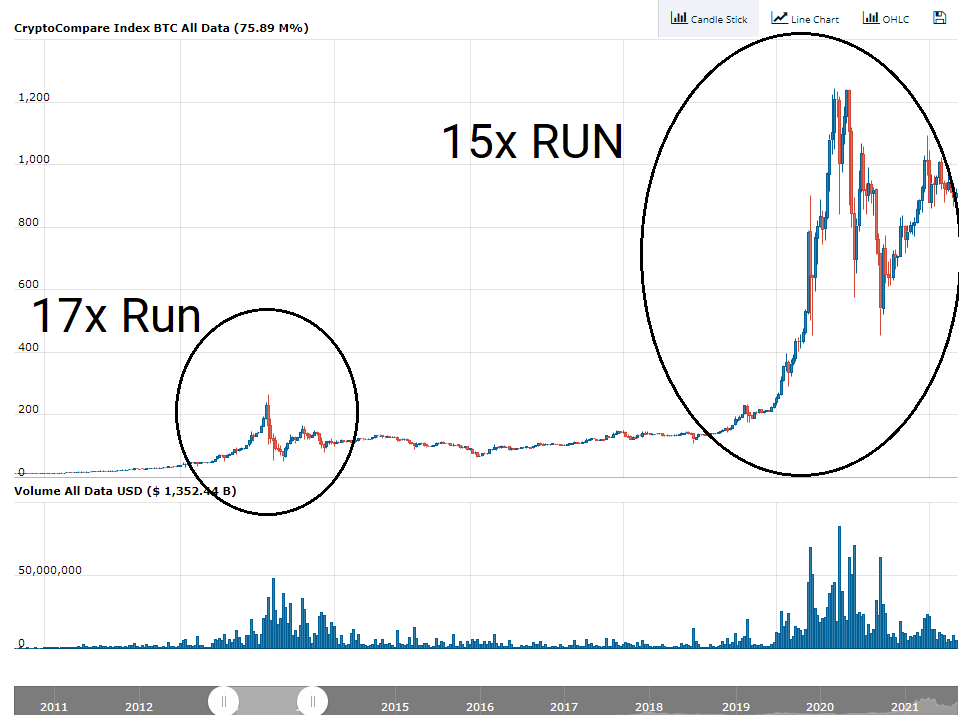

For this strategy’s purpose, “investment risk” is just the “going up and down of coins,” i.e., their price volatility. Cryptocurrencies are notorious for this and it’s also why they can be quite profitable. Here’s an image of Bitcoin’s craziest year on record: 2013.

For the whole year, it did more than 100x and that volatility is great when it’s going in the right direction. It helps you build the sort of wealth that’s the point of The Art of The Bubble.

But if you plan to live on that kind of investment, stuffing 80% declines when you need to take money out isn’t ideal.

The fix here is simple: don’t actually invest in coins. Instead, try to find a “coin neutral” strategy.

Michael Bloomberg is the billionaire who runs the Bloomberg corporation—their exchanges and trading software. He does invest, but he made his main money by getting a cut of other people’s activities using the stock market.

You want something like what Bloomberg does.

Financial Risk

The next kind of risk is the set of variable rate returns you get for staking crypos. Even if you deposit your money on a simple lending platform, like NEXO or Crypto.com, the amount of money you get back is variable.

It tends to go down when people are scared because the oversupply of lenders drives down the price for borrowing. That’s why LEDN rates were 12% in May of 2021 and right now they’re 8.5%.

That’s a problem because if you are counting on a specific amount to live on, a drop of 33% of your expected income won’t be fun.

The fix is simple: build in a margin of safety. If your strategy still works with a 33% drop in expected returns, you have a lot of safety.

So, while we’re only expecting 40% APR, we’ll be looking at an approach that presently yields in the high 50% to low 60% range.

Platform Risk

In this series, I’ve already discussed the main kinds of platform risks that exist (See Lesson 3). They include hacks, coding errors and concept implosions.

That’s a problem because if you have all your money on one platform and it implodes, well there goes your retirement.

There are two fixes here: diversify your platforms and buy insurance. Yes, there is crypto-insurance now and it’ll probably cost about 4% to 6% of your total portfolio a year. You just need to factor those costs into your plan.

So, now we know both the caveats involved and the risks that our strategy will have to navigate. Let’s turn to the strategy in a stepwise way.

Step 1 - Familiarizing

Before you do any of this, you’ll need to familiarize yourself with the basics of transferring and moving money around in the crypto world. It’s not particularly difficult, but it’ll require about 10 hours of upfront work.

And if you want a technical expert to walk you through this, just pick the Technical Support option here.

You need to know about the following:

Getting a browser wallet like MetaMask installed into your browser. Here’s the link for Chrome and it has its own little tutorial video with it.

How to transfer money out of your centralized exchange (where you initially bought your coins) to your browser wallet. Your exchange (e.g. Binance or Coinbase) will have tutorial videos on YouTube for how to do that. Watch them.

How to “bridge” your coins. Basically, you’ll need to move your coins from one protocol over to another. This seems scary at first, but after a bit, it’s like learning to drive a stick shift in a car.

Here’s a link to a video to bridge from Ethereum to Terra (the rest of the video talks about Anchor and you can ignore that). Here’s a link for how to bridge from Ethereum to the Polygon network. They’re imperfect videos, but a good start.

You should know about yield farming generally. So, it’ll be worth your while to read through the previous lessons in this series.

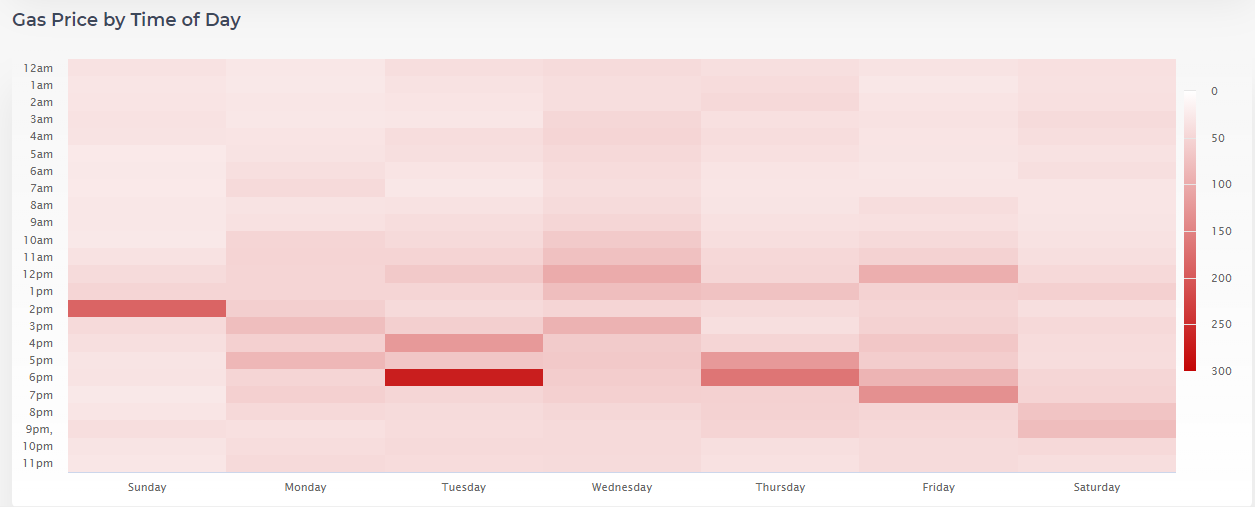

Finally, you need to know a bit about “gas” fees.

Not physical gas, of course, but crypto “gas.” The Ethereum network burns a little bit of Ether for each transaction but does so by way of utilizing another unit called a Gwei. The reasons for this turn largely on the need to tamp down on wild price swings, but they are still pretty big.

The only thing you really need to know is that the more demand there is on the network, the higher the fee. Just like congestion on a highway, though, you can avoid a lot of these fees (and long wait times) if you transact at the right time of day.

Here’s a chart of the current times when fees are high for Ethereum (click the link for updated times in your area of the world).

Since quite a few of the steps involved in this process will require interaction with Ethereum, you can keep your transaction costs down considerably simply by transacting at the right time of day.

I’ll put together a full video for how to do this eventually—I just have a book contract due and I need to finish that up first (I am still a university professor after all).

Again, if you want a walk though, I have a Technical Support plan here with a team of people ready to help. You can also contact me (and team) at theartofthebubble@gmail.com and join us on Discord.

Ok, let’s assume the execution details are under control. What are you going to do?

Step 2 - “Delta Neutral”

In a previous lesson, I outlined a great strategy for earning interest by providing liquidity for synthetic stocks. These synthetic stocks are coins on the Terra blockchain that represent (synthetically) the value of real stocks and exchange-traded funds (ETFs).

By “providing liquidity” I mean that you deposit crypto money on the platform and you earn fees when people buy and sell the stocks. Basically, you get to act like Fidelity for a little bit.

Not surprisingly, this fee-earning strategy can make a lot of money—it’s like Bloomberg. If you do it right, it’s also unrelated to the direction of the stock you’re providing liquidity for.

Here’s how you do it.

Start by buying UST. That’s a stable coin for the US dollar on the Terra blockchain. It is NOT Tether (USDT). UST is available even on Coinbase.

You’ll probably end up buying wrapped UST (wUST) actually—which is the representation of UST on the Ethereum protocol—so you’ll need to do a little work.

Next, withdraw that wUST to your MetaMask wallet. Now head on over to eth.mirror.finance and connect your wallet. Then hit “My Page.” You’ll get something like the following.

Click on the circle with three dots under “Actions” and hit Send.

At this point, I’m going to assume that you’ve also installed the TerraStation wallet as a browser extension. Do that here. Copy and paste the address for your TerraStation wallet in and hit send again (you don’t need a memo).

Wait nervously for about 8 - 15 minutes.

After your money arrives, you’re going to head over to terra.mirror.finance, connect your TerraStation wallet and then buy some synth stocks.

If you have $10,000, for example, then divide that in half, and buy $5000 of a synthetic stock. Hit “Trade” on the left to buy these stocks.

Which stock?

Well for the reasons outline in Lesson #5, you want it to be “Delta Neutral.” Basically, you want the price movement (the delta) to be about neutral over the next 12 months. (Also note, this is not the real meaning of a delta neutral strategy, but it’s close enough).

Paid subscribers get to ask me questions about which stocks my algorithms suggest will do that, and I give them a breakdown of my portfolio exactly so that they know which ones I’m choosing.

Your goal is simply to pick a stock or ETF that isn’t likely to move more than 25% over the next year (up or down).

Now buy that stock and after the process clears hit “Farm” (to the left). You’ll get a screen that looks like this.

You are going to “long farm” and you’ll have to supply both UST and your stock (1 half each). You should also keep about $10 in your account worth of UST for any transaction costs.

As a note, for this approach, short farming is not going to be ideal, since you could be liquidated if prices move too much and our goal is to eliminate as many risks as possible. Also, long farming the VIXY is also not ideal as it’s bound to decline over time. For reasons that are waaaay too complicated, liquidity providing for volatility ETFs is super complex and risky.

I would avoid it unless you understand at least why the VIX number divided by the square-root of 12 gives you the implied volatility of the S&P over the next month.

Now, this approach will pay you your 40%+ APR in MIR tokens. If you don’t want to invest in MIR (and that is the point of this approach as opposed to Lesson 5), then sell them quickly. You’ll have some transaction costs, notably, but because you’re on the Terra blockchain, they’re usually only $.10 - $.50.

After the terra.spec.finance system completes its audit, you might want to go over there to stake your coins instead. The SPEC platform about doubles the APR you get on Mirror presently, but right now it’s risky. After the audit, I expect the returns to go down to probably just 6% - 9% more than Mirror in the future, but it’s still more for doing the same thing.

So, with this, you’ll make about 40% - 60% APR. You’ll need to monitor what’s going on, and you’ll need to select a few “delta neutral” stocks.

At this point, you are in principle done.

The problem is that you might still want to mitigate platform risk. Part of doing that is to diversify your approach and part is to buy insurance. Let’s talk about both briefly.

Step 3 - Diversifying

In Lesson #5, I also pointed out that you could look at Bancor’s platform at bancor.network. To do this, you’ll need to buy BNT (probably from an exchange like Coinbase or Binance) and withdraw that to your MetaMask wallet.

Then head on over to Bancor and connect your wallet. You’ll want to pick something with a higher yield than 40% and with a relatively high 24-hour volume. The ETH/BNT pair works for this. So hit the + sign under actions for that (see image).

This is all runs on the Ethereum network, so be sure to check those gas fee times as you’ll need to make 2 transactions and they will be expensive (I’ve seen $100 + for these).

Deposit your money and wait 100 days. Then you can withdraw your tokens and restake or sell some. The downside to this approach is that you are staking BNT and getting paid in BNT. The getting paid part isn’t much of a problem, because you can always convert those into dollars (or whatever) by selling them immediately.

The real problem is that you need to stake BNT and will be getting a percent based on the value of BNT. Since this is the only platform in the world to have solved the “impermanent loss” problem (read the explanation here), this should work out ok.

But it does involve some investment in a coin, namely BNT, even if in a limited way. So it’s not ideal. In that regard, it’s not too much different from liquidity providing ALCX for the ALCX Pool or CAKE on the AutoCake Swap. Where it’s different is in its actual mechanism (I also understand it a little better and so have more confidence in it).

Let’s look at a last case, then, where you earn a little less in yield but stay out of this coin investment stuff altogether.

Alternative Diversification

One point that people often don’t recognize about Warren Buffett is that he made a lot of his money through insurance. Berkshire Hathway owns Geiko. As he writes in his letters to his investors, this business effectively gave him “free money” to invest with. That’s how he got so rich.

You can do the same thing now with cryptos.

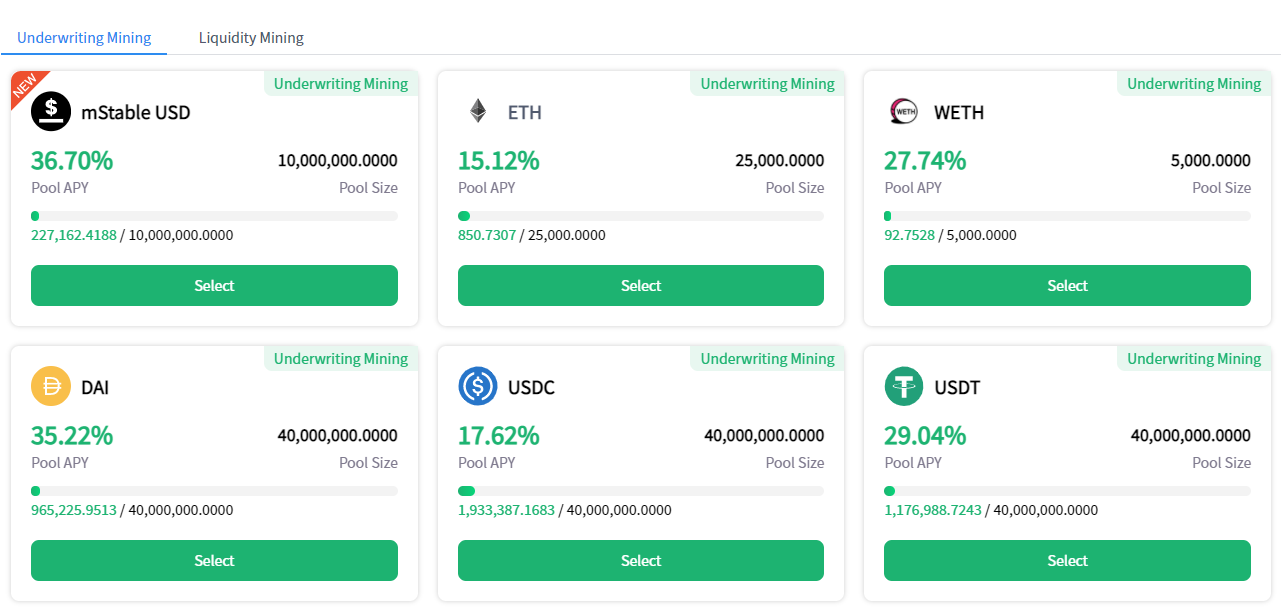

There are a few insurance platforms presently available and in order to function, they require crypto liquidity. InsurAce.io has the most intuitive platform to do this with. You go to the site, launch the app, connect your wallet and pick underwriting mining (at the top of the page).

You’ll get a page that looks like this. Select an option, DAI for example, and check that you understand the risks involved. What you are doing is providing money if there is a smart contract failure for one of their insured services. If a claim goes terribly wrong, then they will withdraw from the reserve amount and could withdraw into your pool. That’s the risk.

Hit “Unlock” and pay the ETH fee (again). You’ll need to leave your money there for 15 days before you can withdraw it.

This doesn’t pay quite as much as the Delta Neutral strategy, but it is still quite good. In fact, if the Spectrum protocol turns out well, then you can combine that with this strategy and still get better than 40% APR.

You’ll need that extra little bit for the next step.

Buying Insurance

Finally, you might want to mitigate some of the platform risks associated with this process. Since the Mirror protocol is fairly important, you could just go buy insurance for it on InsurAce or some related insurance platform.

Unslashed.Finance offers probably the widest array of insurance options, but you can also look at Nexus Mutual and Bridge Mutual too.

Aim to spend 4% - 6% of your portfolio on insurance—especially if you are doing this for retirement. These make sure that if the platforms are hacked or the software malfunctions then you are protected for at least most of your funds.

Concluding Thoughts

Well, this lesson turned out longer than I thought it would, but I think I delivered on my promise.

Crypos can help people in two of the three main financial phases of a person’s life. In the first phase, unless you inherited wealth, you will have to exchange your time for money (called a job or a career) and pay down debts you accumulated along the way.

In the second phase, you’ll have to use your free cash to build wealth. You can, of course, do some of this in the first phase too (this is what retirement plans normally do).

In the final phase, you use your accumulated wealth as a source of “passive,” or better low time investment, income.

Traditional wisdom says that if you take out 4% a year from your accumulated wealth, you’ll be able to live on it indefinitely. Most people don’t get enough money to do that. You need $2,000,000 to earn $80,000 annually that way.

The Art of the Bubble, in its conception, is meant to help people acquire the tools to get through that second phase—the wealth accumulation phase—as fast as possible. I have been doing better than the 100% compound annual growth target so far. Cryptocurrencies are just one tool in my tool kit, but they are a useful one.

What I didn’t expect was that cryptocurrencies, and decentralized finance in particular, would prove so apt for that final phase—the retirement phase. Even just using lending platforms like Crypto.com, which offers 13.5% annually or Anchor, which offers about 19% - 20% annually, drastically reduce the amount of money you need to retire.

At 10% APR, you only need $1,000,000 to retire on $100,000 a year. That’s half as much money as conventional wisdom suggests and it gives you 25% more to live on a year.

At 20% APR, you only need $500,000 to retire on $100,000 a year. That’s a 4th as much as conventional wisdom suggests with that same 25% bump in annual spending cash.

This wouldn’t be The Art of The Bubble though if I couldn’t find you a way to double those numbers.

So with the present strategy, at 40% APR, you can have just $250,000 for retirement and live on $100,000 a year.

For anyone who is at least a DIY-er, you’ll be getting further updates with this approach. The area is fast evolving and it needs regular monitoring.

For everyone else, I hope I’ve shed some light on a useful approach to early retirement.

That’s it for this week! Happy Trading!!

Disclaimers

General financial disclaimer: This post is provided for entertainment purposes only. I am not giving you financial advice and I am not a financial advisor. You should expect no financial returns one way or another based on my statements. These points hold equally for any statements that could be attributed to The Art of The Bubble or any related business entities. If you decide to buy or invest in anything, then your returns and potential losses are your own. No statements about taxation are taxable advice and you are encouraged to consult your own tax professional. You are also encouraged to do your own due diligence before investing in anything.

ooof...