The Secret to Earning 50% APR for Borrowing Money

Lesson 6 | Leveraged Recursive Yield Farming

A friend from graduate school recently asked me about my Bitcoin trading strategies and I told him that I’ve been focusing on crypto yield farming lately because we’re in a crypto-winter.

“It’s basically like earning interest on a bank deposit, but it’s variable interest and takes more steps,” I explained.

“What’s the advantage of doing that?” he asked. “Well,” I said, “I began by borrowing money from one protocol that paid me better than 50% APR to borrow, then I’ve been re-investing that in synthetic assets to earn even more money. You can’t do that with a bank.”

“Wait. You get paid to borrow money?” was his immediate reply.

Yes. You really can get paid to borrow money, for a limited time at least. My friend, who has tens of thousands in student loan debt even after securing a top position at a large commercial bank, couldn't wrap his mind around that idea. Instead, our conversation drifted off to the topic of regulating synthetic cryptos.

I don’t blame him.

I initially had the same response to Anchor’s payment system. When I first took out a small loan, I was getting paid 150% APR. Now, it’s down to about 50% APR. This is, in short, an adoption incentive.

But even if I earn nothing from borrowing, a free loan solves a significant problem in the cryptocurrency world. In Yield Farming Lesson #4 I covered the basic ways to introduce leverage into the crypto world.

Brief recap: it’s doable, but tends either not to scale, or to be very risky.

The reason for that turns on the impossibility of introducing credit scores across blockchain applications without know-your-client (KYC) and anti-money laundering (AML) rules. Put differently, you can’t do it in a decentralized way. Wing Finance, which is trying to introduce credit scores, is doing this by having people register their wallets in a centralized platform with identity verification.

The one, quasi-exception to Lesson 4 enters with recursive yield farming. You can combine that with leverage external to the crypto-world to get even better returns, provided that you understand your risks.

The point of this lesson is to explain one such opportunity, with the hopes that you’ll be able to spot another one if you find one.

If you’re a paying subscriber, you can ask questions about other such possible opportunities on Discord, and all three levels of subscribers (DIY-ers, Crypto Riders, Bubble Riders) will get news of any new such opportunities I find.

As the Decentralize Finance (DeFi) world of cryptos grows, I expect to find more such opportunities. They always have really nice initial yields, which decline over time. So, learning about them early is how you can get 100%+ APR for borrowing. We’ll also discuss how to reinvest that amount for even higher returns.

An entire year’s subscription for The Art of The Bubble at the highest tier costs about 1/5th of most American university courses. So, this one free lesson might well repay that cost. What paying subscribers get is access to my algorithms to maximize returns, which in the cryptocurrency world often do better than double results.

To explain, let’s start with a simple example of recursive farming that has a problem we’ll want to avoid.

Alchemix Recursive Farming

I featured Alchemix’s platform in the first of these lessons. My reason then was that they offered enormous yields for their tokens. But now we have reason to return to them.

One of the primary features the platform offers, and this is the idea of financial alchemy that gives the platform its name, is that you can borrow loans without ever paying that back. Sounds too good to be true, right?

Well, it is. Here’s what they actually offer, just have a look at this image from their site.

What you can actually do is deposit the stablecoin DAI on their site. They’ll then let you borrow half that amount in their own stable coin (alUSD) and never need to pay back that 50% borrowed. In three or so years, since the platform restakes your principle and earns money for you automatically, the loan pays for itself. Then you can borrow another 50%, and so on.

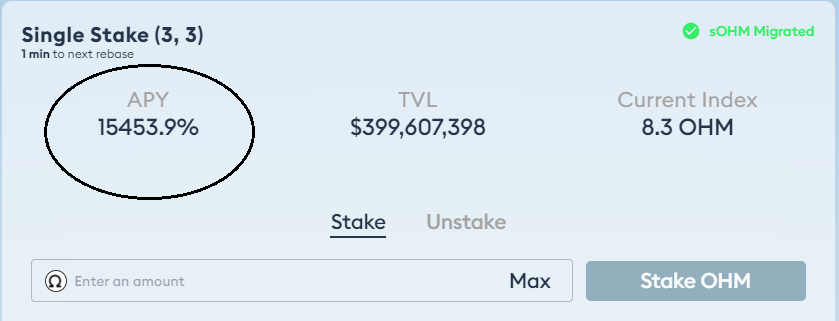

After borrowing once, you could do recursive yield farming. Let’s look at how that would work. Say you deposit $1000 of DAI on Alchemix and borrow $500. You then take that $500, and go to the Uniswap exchange, and buy Olympus (OHM). This is an algorithmic stable coin, and if you are a paying subscriber, you might have already read that I have been farming this thing for a bit.

It started with 15,900% APY yield, but has dropped to 15,400% at the time of writing. It’ll probably drop to a more reasonable amount soon (e.g. 30% APY). Here’s an image.

I’ve only put a little bit into this because algorithmic stable coins have a long history of imploding. If someone finally figures it out, then it’ll be amazing, but those odds are long. My base expectation for this trade is 100% loss.

But risks aside, let’s suppose you decided to do this and managed to get 100% APY for a year’s worth of staking. Well, at the end of 1 year, you’d have $500 on top of the $500 you borrowed, effectively doubling your initial investment money. You could then take that new money and go trade something else.

That process, depositing money, borrowing against it, then depositing again is recursive yield farming. You probably have one obvious question now.

But why?

Why get that 100% APY yield on 50% of your funds when you could get 100% APY on 100% of your funds? To use specific numbers, wouldn’t it make more sense to get a 100% return on $1000 than a 100% return on $500?

Generally, yes. But this approach might offer some insurance. If your $500 in OHM implodes, in 3 years Alchemix will give you that $500 back. On the other hand, that’s not a great kind of insurance, since you need to wait 3 years for replacement.

This is the basic problem of trying recursive yield farming within the crypto-world: because there is no credit on crypto-blockchains, rather than add leverage, almost all loans reduce leverage.

They have to do that, because they need at least 2x collateral if something goes bad with your loan. How else can they recover lost funds?

But, there might be an answer on some platforms.

Luna Borrowing

I wrote about the Terra (LUNA) blockchain in explaining a rational approach to trading moonshots. Theirs is a rival blockchain to Ethereum.

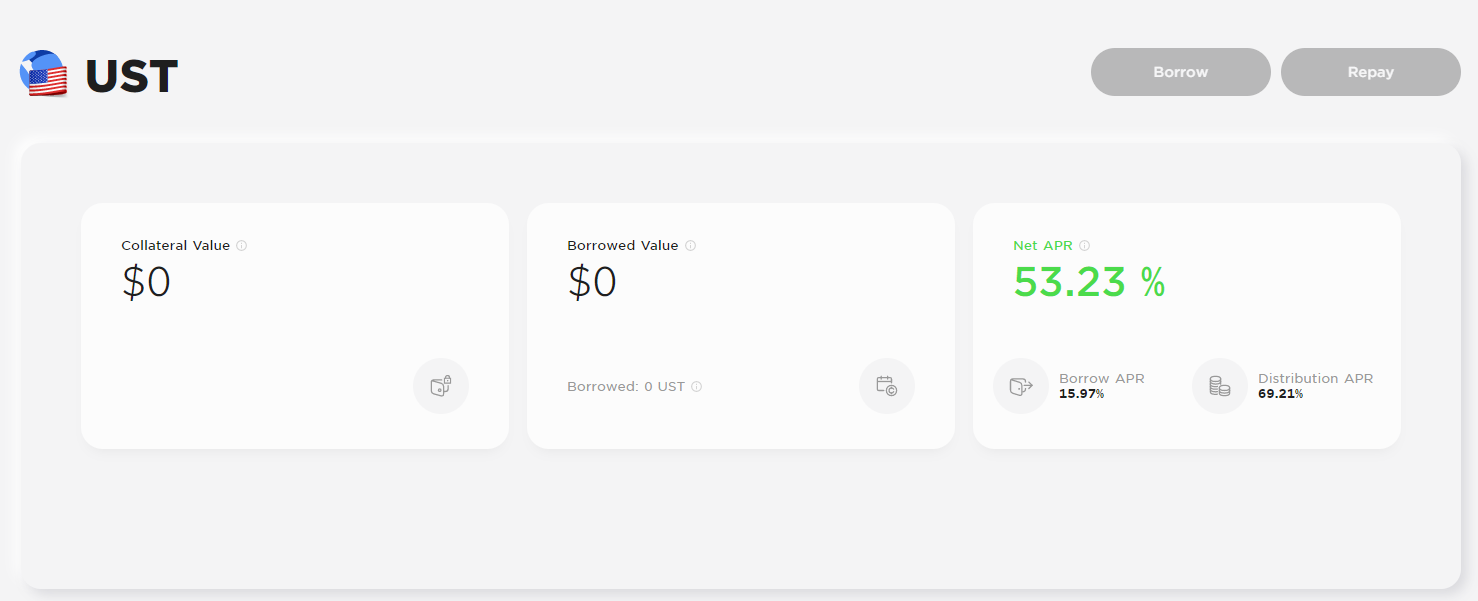

Anchor is the lending and borrowing platform built on the Terra blockchain. You can either deposit their stablecoin, UST, and earn 19.5% APR on that, or you can deposit LUNA coins and borrow against that.

Let’s suppose that you choose to do the latter and deposit $3000 worth of LUNA on the Anchor platform. When you borrow, you’ll actually get paid (see image below).

Yes, you get paid in Anchor tokens, which aren’t worth a lot. But you are getting paid, which is interesting.

Additionally, you also get the UST you borrowed to go do whatever you want with--it can be about 33% of your deposited amount. So, now you have $1000 borrowed dollars.

Since everything on the Terra blockchain is cheap, you might as well send it over to the Mirror protocol where you can buy synthetic stocks, coins, and other items. Here are a few of their farming options.

To take advantage of this, you could either just buy synth stocks like Galaxy Digital and hope they go up.

Or you could decide to farm them in the way that I described in Lesson 5 -- turning dead money into nice yields. This means that you might buy $500 of USO, which is unlikely to go up more than 25% over the next year, and stake that with another $500 of UST. That way your total deposited amount is $1000.

If yields remain about the same, you’ll earn roughly $300 on that. Oil is likely to go up, so you might earn maybe another $100 too. Finally, you’ll earn another 50% in Anchor tokens on your LUNA (= $1500), and whatever amount your LUNA tokens go up. So, $1900 on top of your gain in LUNA (= 63% better).

That’s the smart way to do recursive yield farming.

What’s The Catch?

One possible problem with this approach is that LUNA might drop a lot in value. You are, principally, investing in LUNA with this strategy. My algorithms personally help me know when to buy and sell, and my subscribers get access to that. You will need some system of proven trading signals to do this intelligently.

Even still, the yield farming earnings that you’ll make on this provide some insurance against a LUNA drop, so in that regard, this strategy actually lowers your financial risk.

As I see it, then, there are three main problems here.

First, these rates are variable and you might have to close up shop early if the yields fall too much. Second, you’ll also need to watch to make sure that LUNA doesn’t drop below your liquidation value (45%), or else your deposit will be liquidated (financial risk). Finally, you are hoping that the various platforms survive or aren’t hacked (platform risk).

Here are some thoughts for dampening those risks. First, the Anchor platform is still new, but because it’s relatively simple in structure, that gives me confidence that its platform risk isn’t too great. Still, I’m keeping my exposure limited.

Second, the suggested borrowing rate, at about 33% is even lower than Anchor itself suggests as safe, so that’ll lower your probability of liquidation. And you’ll see that coming. The platform gives you alerts if you are too low, and you’ll be able to sell and repay if necessary. If you really had to, this is where you might use a line of credit to temporarily shore up your account.

Finally, the variability of the rates earned isn’t that unpredictable: they go down over time. You can’t really build a business on that, but it does tell you how to structure your trades.

Those points notwithstanding, what you have managed to do is leverage your returns within the cryptocurrency world. The only way that’s possible is if you can borrow against your own money and earn money on that borrowing, or if you can borrow against a coin that isn’t a stable coin, or (as we’ve done in this case) both.

The Anchor platform solves the basic problem we ran into with the Alchemix approach.

Concluding Thoughts

Of course, this strategy only introduces about 60% internal to the blockchain system, assuming that everything goes about as planned.

One way to improve on your returns might be to move your borrowed money back onto the Ethereum blockchain and stake that at Olympus (OHM) to get that 15,000% APY. Or, you could buy Ethereum itself in phases--crash cost averaging your way in. Finally, you could always add leverage to your trade using the methods discussed in Lesson 4.

That’s how you can do recursive yield farming with leverage. I expect more such opportunities to emerge as the race to establish DeFi dominance continues, and to all my paid subscribers, you can be sure to learn about those as they emerge as new possibilities.

To recap on this mini-series: yield farming not only makes sense as an investment strategy in its own right, but also can significantly boost your returns during a crypto-winter.

Overall, in this crypto-winter, I’ve been earning on average about 40% APR moving my yield farming funds about. My subscribers have received reports on this weekly. Since The Art of the Bubble’s target is 100% each year for any 5 year period, earning that additional amount while I’m waiting makes that goal significantly more achievable.

That’s all for now! Happy Trading!

Disclaimers

General financial disclaimer: This post is provided for entertainment purposes only. I am not giving you financial advice and I am not a financial advisor. You should expect no financial returns one way or another based on my statements. These points hold equally for any statements that could be attributed to The Art of The Bubble or any related business entities. If you decide to buy or invest in anything, then your returns and potential losses are your own. No statements about taxation are taxable advice and you are encouraged to consult your own tax professional. You are also encouraged to do your own due diligence before investing in anything.